There are Two People. Which one do you Select?

Why Normalization Feels Cold — and Why That’s When Decisions Matter Most

I was on what we used to call the buy side in the late 1980s and through the 1990s—what today would be labeled private money management, private equity, or investment advisory work.

We bought and sold companies. I was part of a group that managed bank trust and private accounts totaling more than $4 billion, and at 26 years old I was named the youngest Senior Vice President in the history of the National Bank of Commerce in Memphis. That didn’t happen in a vacuum. Myron and Alex took a young man seriously in 1987 and 1988 and taught him how to think.

At the time, I managed a money market mutual fund and handled daily funding for some of the largest companies in the country through 30-, 60-, and 90-day commercial paper and overnight repos. I loved the work. But more importantly, I learned something that has stayed with me ever since.

There are two kinds of people you can use in decision-making.

The first has an opinion and is mostly right. When Alex thought we should pursue something—Rhodes Furniture, HBO & Company—you didn’t overthink it. You acted. The odds were strongly in your favor.

The second has an opinion and is mostly wrong. Surprisingly useful. Do the opposite of what they suggest and you’ll often do just fine.

What you cannot use is someone with no opinion at all.

That brings me to real estate.

Many agents—even very successful ones—are winging it. They may be good salespeople, but sales success is not the same thing as decision quality. The real question isn’t how many transactions someone closes. It’s what results they leave behind.

I ask that same question of myself. I’m an economist by training, and I track every transaction our team completes to understand whether it was the right move—not just emotionally, but financially.

On the sell side, exits are easy to evaluate. On the buy side, the bar is higher. Did they love the home? Good. But how did it perform?

Across more than 307 transactions, only three have resulted in a loss for our clients. All three occurred in 2025 and stemmed from purchases made during a more optimistic phase of the market. One was a new build that simply couldn’t deliver the value. The other two were intentional losses—capital redeployed into more productive assets due to changing circumstances.

I don’t say that to sound arrogant. I say it to be precise.

Our team doesn’t shy away from having an opinion because we might occasionally be wrong. We look at the long arc of decisions and hold ourselves to a higher standard: being mostly right is what makes you useful.

And that’s why, mostly in private circles, I’m taking some modest heat for saying plainly that this market is normalizing, not collapsing—and that we are holding the substantial majority of the gains made during the pandemic-era run-up.

This isn’t theory. It’s recorded behavior.

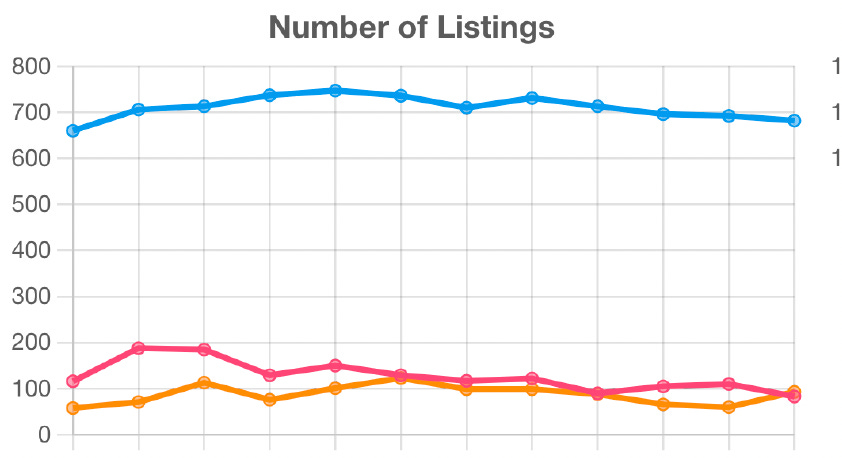

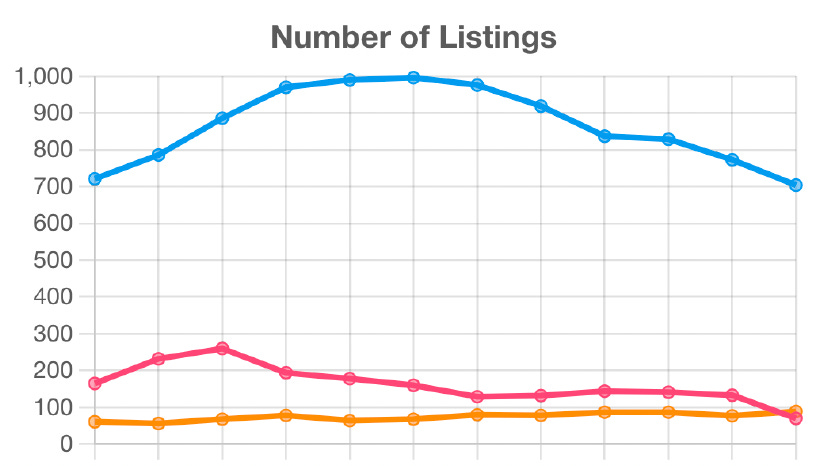

What market is better do you think?

This one above? Or this one below?

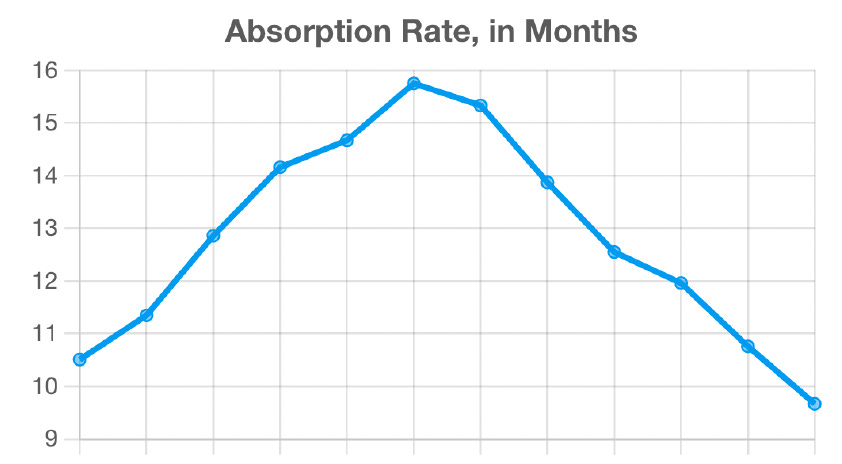

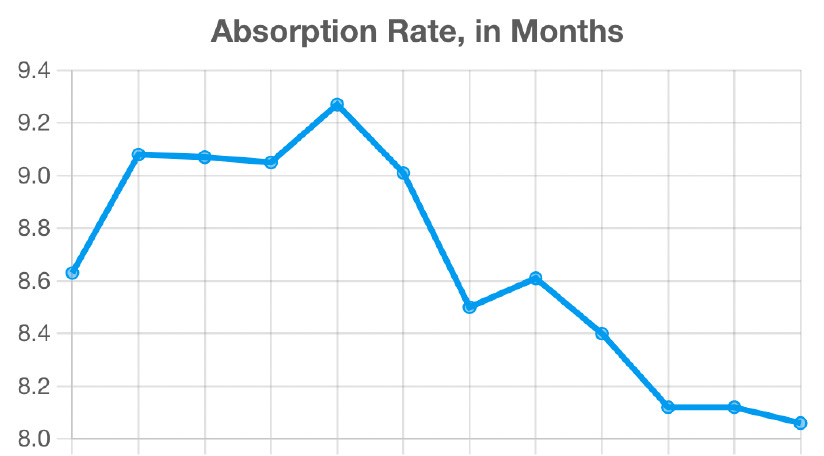

Perhaps this will further assist.

This?

Or this?

Would you think this below is healthier than the one that follows or are they the same?

Or

I defy anyone to tell me which year is which in those charts, or to argue—honestly—that there is a statistically meaningful difference between them.

There isn’t. There is volatility difference here and there to be sure. There is certainly difference of opinion on where we were and where we are. But the data is pretty clear at least for me and our team to be advisors. The market is normal and predictable again. Clear and precise.

What we’re seeing in 2025 is not erosion. It’s normalization. We’ve returned to normal sales unit volume, normal inventory levels, and a set of metrics that look far more like a functioning market than an emotional one.

If I had used 2018 as the base year—and I will begin doing that for 2026 comparisons—the normalization would be even more obvious.

So yes, I have an opinion.

Buy your straw hats in the winter.

And make no mistake—

it is winter on 30A.