Did you Think Losing Money Was OK?

Prospect Theory, Vacation Homes, and Hesitation fot Say "Yes"

There is a category of buyer I encounter regularly — intelligent, accomplished, financially capable — who wants a vacation home and yet never quite allows themselves to buy one.

These are not people stretching. They are not overleveraged. They are not confused about what they can afford. In many cases, they could write a check for the property and never think about it again.

And still, they hesitate.

They will talk about markets. They will reference 2008. They will want a certain price for a specific kind of property and those things do not line up. They will mention maintenance, hurricanes, rental risk, opportunity cost, or the idea that “real estate feels expensive right now.” All of those explanations sound rational on the surface. None of them are the real reason.

The real reason lives in psychology, not finance.

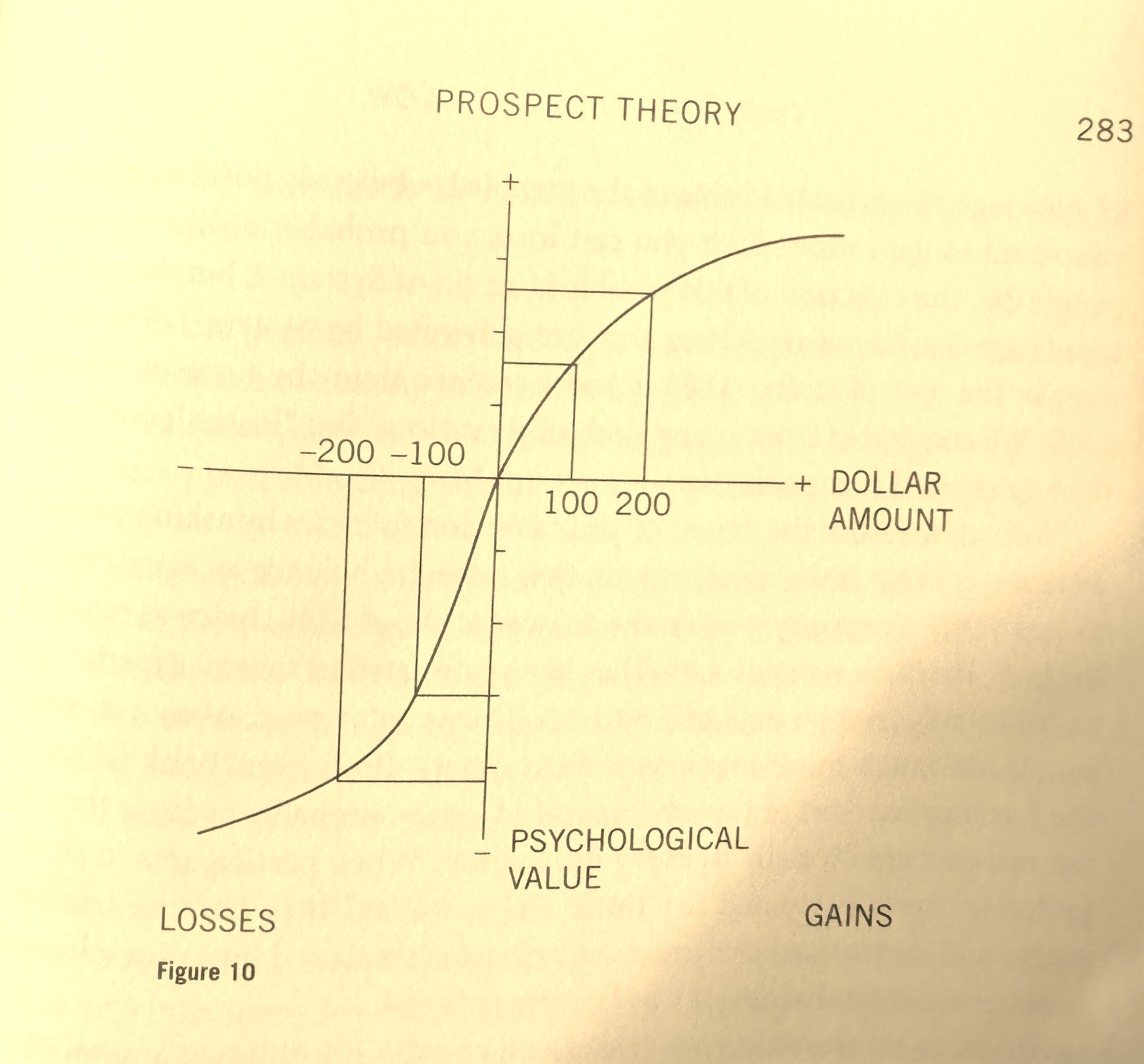

Daniel Kahneman explains it cleanly in Chapter 26 of Thinking, Fast and Slow, where he lays out Prospect Theory — a framework for understanding how people actually evaluate risk, loss, and value.

The short version is this: human beings do not experience gains and losses symmetrically. Losses hurt more than equivalent gains feel good. And once that imbalance exists, it distorts otherwise rational decisions.

Vacation homes sit right in the crosshairs of this distortion.

How Prospect Theory Shows Up in Real Estate Decisions

Prospect Theory tells us three things that matter here.

First, people measure outcomes relative to a reference point, not in absolute terms. Second, losses loom larger than gains. Third, when an outcome is framed as a loss, people become risk‑seeking; when it is framed as a gain, they become conservative.

Now apply that to a discretionary purchase like a vacation home.

The buyer’s reference point is not the life they could live with the home. It is their current balance sheet — liquid, clean, untouched. Anything that moves money out of that state is experienced as a loss or at least a contemplative change, even if it is converted into a hard asset they intend to use.

Ownership costs are therefore framed mostly as losses, not expenses for value and gain.

Maintenance is not upkeep; it is erosion. Property taxes are not participation in a community; they are money gone. Insurance is not protection; it is money spent in fear.

Rental income, even when predictable, is not experienced as a gain. It is framed as a gamble against those losses — uncertain, effort‑dependent, and therefore psychologically discounted.

This is why two buyers can look at the same pro forma and have completely different reactions. One sees a balanced exchange of value. The other sees a slow leak.

The math may be identical. The emotional accounting is not.

The Thought Experiment That Clarifies Everything

When I sense a buyer stuck in this place, I often slow the conversation down and propose a simple scenario.

I tell them: let’s agree, for the sake of discussion, that the home we’re looking at is worth $4,000,000. We both believe that. The market data supports it. You buy it for $4,000,000 and you own it outright. No debt. No leverage. This is not about financing risk.

You use the home with your family. You also rent it occasionally — not aggressively, not obsessively — simply enough to offset ownership.

Let’s say it generates $200,000 a year in short‑term rental revenue, and after all expenses you clear roughly $100,000 annually. We will ignore income taxes and depreciation entirely, because they complicate the point.

You do this for ten years.

Then, ten years from now, your life changes. The kids are grown. The beach no longer fits the same way. The childhood memories created are gone now and “the cats in the craddle and the silver moon” is what has become of your life.

We look at the market honestly, the same way we did on the way in. We agree, and at the closing table, you might walk away with $3,965,000 in cash.

Not $4,000,000. Not a win on paper. A modest loss. It is possible. At least consider that. This goes against the internal story line. But then the question is nearly ready to be posited.

At that moment, after a long pause, I ask a single question:

Will you have been happy?

Why This Question Is So Uncomfortable

For someone not trapped by Prospect Theory, the answer comes quickly.

“Of course.”

Ten years of family time. Ten years of holidays, summers, long weekends, and ordinary days made extraordinary by place. Ten years of optionality. Ten years of a life actually lived. “I’m good with that”.

The money did its job. But for someone deeply loss‑averse, the answer stalls.

They start recalculating. They re‑anchor to the missing $35,000. They mentally erase the rental income as if it never existed. They replay the decision as a financial outcome rather than a lived experience.

In that moment, something important is revealed. They are not buying a home or experience or memories. The finite experience has not yet revealed itself.

They are trying to win.

And vacation homes are not designed for winning in the way financial instruments are. Vacation Homes are designed for use, memory, presence, and time — all things Prospect Theory undervalues because they do not show up cleanly on a balance sheet.

Better to buy stocks and bonds. Mediums of exchange. That is easier to value.

The reality of the story is simple. You would have put $4,000,000 to work, you would have gained $1,000,000 after expenses, and you would have walked away from closing with $35,000 lost on the initial investment. Of course present value of a dollar not considered for ease of discussion, what’s wrong with this for a few sandcastles on the beach?

It is a 25% absolute return on the $4,000,000 over 10 years. Horrible by some standard. And if they get framed in that thought, then well, we are probably done looking for homes.

The Reality Check

This is the part most advisors avoid saying plainly.

If you cannot answer “yes” to that question — if a modest, fully understood, fully affordable financial loss invalidates ten years of meaningful living — then you should not buy a vacation home. Not here. Probably not anywhere.

Because the problem is not the market. It is not the price. It is not the property.

It is that you are measuring life decisions with a framework designed to avoid regret, not to enable joy. Prospect Theory 101.

Prospect Theory is useful for protecting capital. It is terrible at guiding discretionary life choices.

The Path Forward

The most grounded buyers I work with make a quiet shift. They stop asking, “Will this outperform?” They start asking, “What is this money for?”

When the answer is “to support a life we actually want to live,” the math becomes contextual instead of absolute.

A vacation home, a place for life experiences and indeed life experience itself, is not a bet against the market.

It is a bet on your future self valuing time, place, and shared experience more than a perfectly preserved balance sheet.

And if that bet feels wrong, that is not a failure. It is clarity. It is ok and can be rational not to buy the beach house. But as Denzel Washington requoted from his pastor who imparted this wisdom.

Whatever your dreams are, they must leave the realm of dreams and get cast as goals with effort taken daily to reaching the goals that ultimately fulfill the dream. At least that’s my interpretation.

The worst outcome is not losing a small amount of money. The worst outcome is realizing later that you were financially right and existentially wrong.

That question at the end — will you have been happy? — is not rhetorical.

It is diagnostic.

Answer it honestly, and the decision usually makes itself. Our market is a life‑choice market. The sooner that is understand, the sooner we can be comfortable with a beach walk.