I can beat Time and Here is How

The Statement Everyone Makes

There’s a moment in almost every conversation—usually early—where someone says it without hesitation:

“I’m in real estate investing.” Or something like that or Bitcoin…whatever it is we first have to understand what they mean and we have to level the playing field. Let’s do that for real estate “investors”.

They don’t say it defensively. They say it the way someone states a fact, like where they live or what they do. And most of the time, nobody challenges it, because it sounds right. They own property. They’re collecting rent. They’re “in the game.”

But I’ve learned to pause at that sentence, because it hides a more important question:

What are you actually doing?

Not what you call it. Not what you intended. What are you actually doing with your capital?

Because when you slow that question down, most of what people describe as “real estate investing” starts to look a lot less like investing and a lot more like something else entirely.

So rather than argue about it, let’s just walk through it.

Same starting point, same time horizon, no tricks. Just different behaviors and what they produce over time.

Three People, Same Starting Point

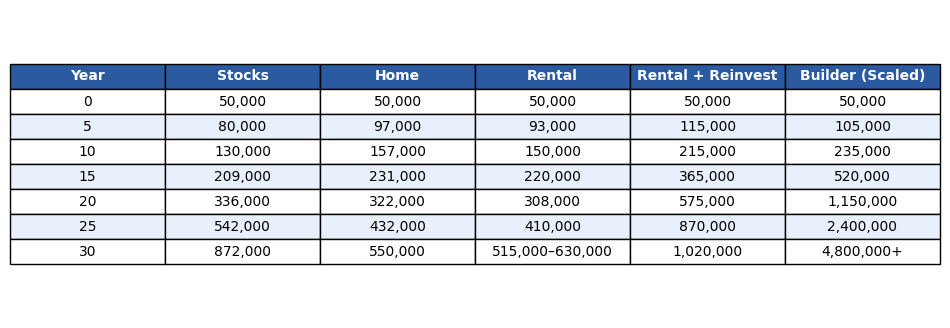

Imagine three people sitting at a table thirty years ago, each with $50,000. They don’t know each other. They don’t coordinate. They just make what they each think is a smart decision.

The Passive Investor (Stocks)

The first person does the least interesting thing of the three. He takes the $50,000 and puts it into a broad market index. No story, no edge, no timing. He doesn’t try to be clever. In fact, the defining characteristic of his strategy is that it doesn’t require him to be clever. He lets it sit, he adds nothing fancy, and over time the market does what it has historically done. Thirty years later, he has something in the neighborhood of $872,000. Nothing dramatic happened along the way. That’s precisely the point.

The Homeowner

The second person takes the same $50,000 and buys a house for $169,000. He moves in. Over the next thirty years, he does what homeowners do. He makes his payments, pays his taxes, replaces things he didn’t know existed until they broke, and slowly reduces the loan. The house appreciates along the way. At the end of thirty years, he owns it free and clear and it’s worth roughly $550,000. He did well. He built equity. But if we’re being precise, what he did was commit to a payment and stay in one place long enough for time to work in his favor. There’s discipline in that, but there’s not much in the way of investment decision-making once the initial purchase is made.

Indeed the analysis is more complicated because money goes in every month for many things and for many years.

The Rental Owner

The third person looks at both of those and says, “No, I’m going to do this properly.” He buys the same house, but instead of living in it, he rents it out. Now we’re in what people like to call “real estate investing.” And for a while, it feels that way. There’s activity. There are decisions. There’s the sense that something is being managed.

But if you actually watch what happens over time, it’s more mundane than the label suggests. Some months the property is occupied, some months it isn’t. Some years the numbers look clean, and some years something expensive interrupts that narrative. If he’s disciplined, he improves the rent over time and maybe even generates a modest surplus. Over thirty years, the loan gets paid down, the property appreciates, and he ends up with something between roughly $550,000 and $630,000 in equity. If he’s more thoughtful and reinvests whatever excess cash flow shows up along the way, he can push that outcome closer to a million dollars. It is not complicated math, but at least he was getting someone else to nearly pay or mostly pay everything. Mostly.

That’s a good result. It deserves to be called that. But it’s also worth noticing what didn’t change.

He bought something.

He held it.

He waited.

The structure is the same as the first person with the index fund. The only real difference is that he inserted himself into the middle of the process. More effort, more friction, more variables—but still fundamentally a strategy that depends on time doing the heavy lifting. What was not considered to make it even more equivalent was to put in place a “property manager” to take nearly 5-15% per year to help manage the property so the “investor” could step away and just watch just like the index fund investor. Leaving that aside, let’s just continue on.

The Problem with the Debate

And this is where most of the conversation about “stocks versus real estate” quietly goes off track. Because by this point, everyone is comparing outcomes and arguing about which one is better, without noticing that they are comparing two versions of the same underlying behavior: put capital to work and let it compound. There a tons of ways to do that and these are just two ways and they are not directly comparable. Just like a Beachfront home at $3,400 per square foot is not comparable to a fixer at $350 per square foot just 1 mile away. Bitcoin is not the same as gold either.

What we are debating is ego.

Still, the stock investor is very hard to beat, and the numbers reflect that.

The Builder Appears - the 4th Person

But there is a fourth person at the table we haven’t talked about yet, and he is doing something that doesn’t look like any of the others.

He also starts with $50,000. He also operates in real estate. But he doesn’t buy a house to live in, and he doesn’t buy one to hold. He buys land, builds a house, and sells it. At the closing table, after costs, he nets about 16.5%. Not on paper. Not as an estimate. In cash. Those costs in this conversation also include the cost of capital acquired from others (Financing).

Then he does something that seems almost too simple to matter.

He does it again…….and again….and…Now we are talking about Velocity of Capital and the Cash Conversion Cycle which is all that matters.

The Shift from Waiting to Turning Capital

The first few years look unimpressive. One project at a time, capital tied up, progress that feels slower than it should. But each time he completes a project, his capital base increases. And because he is not waiting for appreciation, but actually realizing profit at each cycle, that increase is tangible and immediate.

After a while, something changes. The capital is no longer just enough to do one project. It can support two. Now two projects are moving at the same time, each producing its own margin, each feeding back into the same pool of capital. A few cycles later, it becomes three. The timeline compresses from long stretches of waiting into a sequence of shorter, repeatable events: build, sell, redeploy.

At that point, he is no longer participating in the same kind of activity as the other three. He isn’t waiting for value to appear. He is creating it, capturing it, and then deliberately putting it back to work.

If you’re wondering where I sit when I say “real estate investing,” it’s here. Not because it sounds better, but because it behaves differently.

The Outcome

Thirty years later, his outcome doesn’t look like a variation of the others. It looks like it belongs in a different category altogether—on the order of four million dollars or more from the same initial $50,000.

Nothing about the asset class changed. It was “real estate” in all three other cases. What changed was the behavior.

Where the Argument Breaks

And that’s the part that tends to get lost.

Why? Because what most all people are actually doing with “real estate” investing is not fundamentally different from what the stock investor is doing. They are accumulating wealth over time, with varying degrees of efficiency.

When people say that stocks outperform real estate, what they are usually observing—accurately—is that passive, time-based compounding in the market outperforms most people’s experience of owning propert and indeed even renting it out. The reality is they are both “passive” wealth accumulation models and I will go to the mat defending stocks against the typical model, but if you ask me does real estate investing outperform the stock market I will say Yes!

Because the builder is doing something else. He is not relying on time as the primary driver. He is relying on margin and repetition. That introduces a different kind of risk—execution risk, timing risk, operational complexity—but it also produces a different kind of outcome.

The Numbers, Side by Side

No interpretation needed. Just structure and outcome. It baffles me why people that have done this just once do not keep going. Because you know why? They may lose one or two hands at Blackjack along the way.

Final Distinction

So the distinction isn’t really between stocks and real estate.

It’s between strategies that depend on time, and strategies that depend on action.

You can call both of them “investing” if you want. People do. The terminology isn’t the important part.

But the math is.

A Final Thought Experiment

If you want to pressure test this idea, take it out of theory.

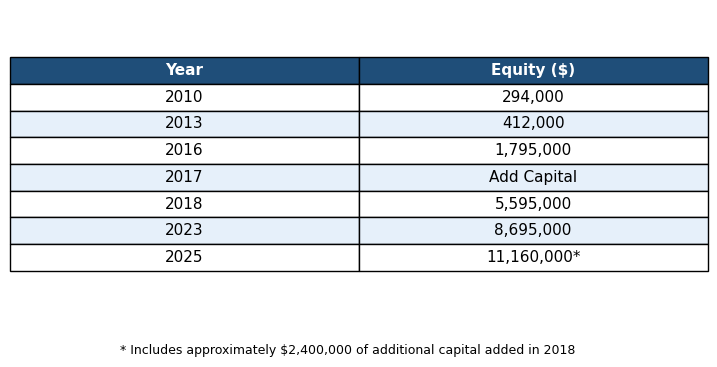

Imagine someone who, around 2010, had roughly $294,000 of equity. Not a fund, not institutional capital—just accumulated equity, and not even all of it, just enough to pursue an idea that at the time may not have fully revealed itself.

Instead of holding property and waiting for appreciation to do the work, they began to build, sell, and redeploy capital. Not in a dramatic or highly visible way, but steadily, repeatedly, and with a consistency that only becomes meaningful over time. The scale was above entry-level housing, yes, but the underlying approach was not complicated. It was the same basic cycle, executed again and again.

Along the way, additional equity—approximately $2.3 million—might be introduced oh lets say near halfway through around 2017. Not as a perfectly timed infusion, but as a continuation of what was already working.

From there, the distinction becomes clearer. The growth that followed was not driven by passive appreciation, nor by simply holding assets over time. It came from iteration—projects completed, capital realized, and then deliberately put back into motion.

Fast forward to the present, and that original $294,000 might have grown for that investor to rather nice levels. Could this happen? Is this one of our investors? Could it be you? The point is this stuff works even if along the way there were maybe three losses.

At that point, the question is no longer whether money was made. The question is whether this resembles what most people are describing when they say they are “investing in real estate.”

Because if the comparison being made is between this and buying an asset and holding it for thirty years, then the comparison itself is flawed.

And no broad equity index, starting from that same point in time and with that same initial capital, produces a comparable result.

That is not luck.

It is structure.

That’s not appreciation.

That’s what happens when capital is turned instead of parked.

Call it whatever you want.

That’s real estate investing.